When the first digital currency was created, there was an immediate need for a way to store and manage it. Thus, the BTC wallet was introduced, acting as a storage tool for cryptocurrencies.

As digital currencies are a unique form of money, they require a special type of wallet. In this article, we will explore the key features of cryptocurrency wallets, their different types, the process of creating and using them, and the essential security measures you need to know.

When cryptocurrency was first created, its goal was to be an alternative to traditional money, but with more advanced features. To some extent, this has been achieved, though cryptocurrency has not yet replaced fiat money. Nevertheless, digital coins are widely used for various transactions across the globe.

Key features of cryptocurrencies

Digital currencies differ from traditional money in many ways. They cannot be touched or physically held. They operate under principles and laws that are completely different from those of conventional currencies. Let's take a closer look at the key features of cryptocurrencies and how they differ from fiat currencies:

- Decentralization: Unlike traditional currencies, which are regulated by governments and their institutions, the issuance and circulation of digital currencies are not controlled by any governmental body or organization.

- Resilience to inflation: Stemming from the first point, unlike fiat currencies, no one can issue additional units of a cryptocurrency to manipulate its value. Cryptocurrency prices are determined solely by supply and demand.

- Anonymity: Transactions are anonymous—only wallet addresses are visible, not the identity of the owners. In contrast, traditional money transfers disclose all the details of both the sender and the recipient.

- Security: Transactions are secured through blockchain technology, where data is encrypted and organized into blocks that are linked in an unbroken chain. Copies of the blockchain are stored on many independent devices rather than on a single server.

- Irreversibility of transactions: Once a transaction is recorded on the blockchain, it cannot be undone due to its structure. Each subsequent block is linked to the previous one, making it impossible to alter one without altering the entire chain.

- Transaction speed: Unlike bank transfers that may take one or several business days to process, cryptocurrency transactions are much faster, typically taking only a few seconds or minutes, depending on the network.

Difference between cryptocurrency and traditional currency

Cryptocurrency was initially created as an alternative to traditional money, aimed at providing faster and safer payments. However, unlike fiat money, digital coins are not yet recognized as legal tender in many countries.

Therefore, cryptocurrencies are largely seen as an investment tool or a means of generating income through trading, investing, mining, and other methods. Fiat currencies remain the standard legal payment method between individuals and businesses.

Below is a brief comparison of digital and fiat currencies:

| Parameter | Cryptocurrencies | Fiat money |

| Regulation | Not regulated by any institution | Regulated by specific governments and entities |

| Issuance | Usually limited (set when currency launches) | Unlimited |

| Electronic form | Exists only in digital form | Can be converted into physical form (cash) |

| Counterfeiting | Impossible | Possible |

| Exposure to inflation | No | Yes |

| Confidentiality | Yes | No |

| Security | High (secured by blockchain technology) | Low (banks are often targets of cyberattacks) |

| Reversibility of transactions | Irreversible | Can be canceled or reversed |

| Transaction speed | High (some chains process in seconds) | Low (can take several days) |

| Transaction fees | Low | High |

| Storage | In specialized crypto wallets | In bank accounts or physical wallets |

BTC wallet

As we noted earlier, the key difference between digital and traditional money is that the former has no physical form, so you cannot hold or touch it. Even when we receive traditional money electronically, such as a transfer to a card, we can withdraw it and put it into a wallet.

Cryptocurrencies, however, cannot be physically withdrawn, but a wallet is still needed to store them. So, what exactly is a cryptocurrency wallet, what types are there, and how do they work? And which BTC wallet should you choose? We will explore these questions in this section and those to follow. Let’s start by defining what a cryptocurrency wallet is.

A cryptocurrency wallet is a special program or device designed for sending and receiving digital coins. In reality, cryptocurrencies themselves are not stored in the wallet. Instead, the wallet stores the keys that provide access to the digital currency. To simplify this concept, let’s draw an analogy to another familiar tool.

We are all familiar with bank cards, and just as money is not physically stored on these cards, cryptocurrencies are not stored in wallets. However, these cards give us access to our accounts, enabling us to send money to others, pay for goods, and more. But the card itself is just a tool to access the money.

All transactions with traditional money in electronic form, as well as with cryptocurrencies, are carried out in virtual space. In fact, money is not physically transferred; instead, records are made that the sender transferred a certain amount of money to the recipient, the sender’s account is debited, and the recipient’s account is credited.

Without a wallet, it becomes impossible to perform any transactions with Bitcoin or other digital currencies, whether sending, receiving, or storing coins. As a reminder, the wallet does not hold the coins themselves but only the access keys. Let’s dive deeper into how this works.

How it works

So, how does a cryptocurrency wallet function? Before you fund your Bitcoin wallet, it is important to understand how it works and what data it stores. Cryptocurrencies and the addresses where they are stored are controlled by the blockchain, and to confirm ownership and manage the coins, you need keys stored in wallets.

A key is a unique sequence of numbers and letters from the Latin alphabet. When using wallets for digital currency transactions, two keys are employed: a public (or open) key and a private (or secret) key.

A public key is the address of the wallet to which other users can send cryptocurrency. It works much like a bank account number. This address does not need to be hidden and can be shared publicly. Public keys can vary in length, ranging from 52 to 130 characters, with shorter addresses being the most common.

A private key is a code that grants access to the assets in the wallet, similar to a safe combination or a bank vault key. It is confidential and should never be shared with anyone. When performing transactions, a digital signature is used that is created using the private key. Without the private key, it is impossible to perform any cryptocurrency transactions.

If the private key is lost, the user will no longer have access to their crypto assets. However, there is one way to recover access to the wallet—through a seed phrase. This is a list of random words (12, 18, or 24 words) used to restore assets if the password to the application or device storing the wallet is lost.

It is recommended to store this seed phrase either encrypted on your computer or simply written down on paper. However, even this method of storage is somewhat risky. After all, paper can be lost, torn, or accidentally thrown away with other unwanted documents.

Types of wallets

There are various classifications of crypto wallets. One of the most common and easy-to-use is the division into hot and cold BTC wallets. Each has its own advantages, as well as pros and cons that should be considered before making a choice.

A hot wallet is connected to the Internet, allowing its owner to conduct cryptocurrency transactions from anywhere in the world. These wallets are free and perfect for everyday use such as trading. However, they come with a significant drawback—limited protection against hacker attacks.

A cold wallet, on the other hand, is typically a separate device, similar to a USB drive, that does not have constant access to the Internet. This makes remote theft of cryptocurrency from these wallets much more difficult than from hot wallets. They are perfect for long-term storage of coins such as for investment purposes.

Wallets are also categorized as custodial or non-custodial wallets based on how private keys are stored. If the user personally stores the private keys and is responsible for their safekeeping, the wallet is considered non-custodial. This includes all hardware wallets and some hot wallets.

In the case of custodial wallets, the keys are stored not by the asset owner but by the service providing access to the assets. A major advantage of these services is that if a user loses their password, they can contact customer support to regain access. Such services are often provided by crypto exchanges, brokerage platforms, and others.

To summarize, here are the main types of wallets:

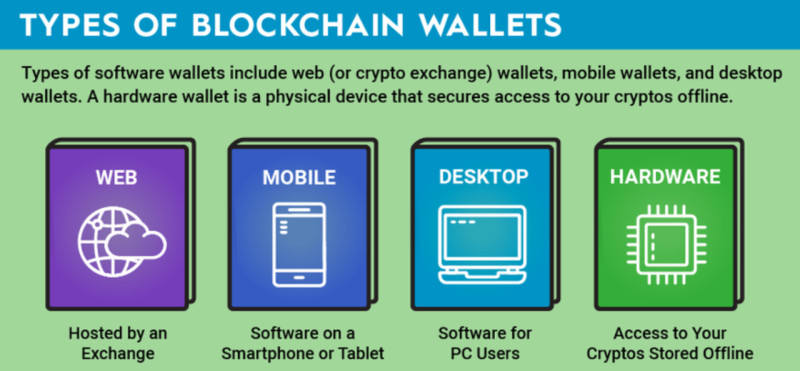

- Online wallets are web services that operate through the Internet and store keys on their servers. These can be accessed anytime from any device and are often used by crypto exchanges.

- Desktop wallets are programs installed on a desktop computer or laptop that store the keys on the device itself.

- Mobile apps are wallets used on smartphones, allowing transactions directly from the phone. While convenient, losing or having your smartphone hacked can result in a loss of access to your assets.

- Hardware wallets are special devices that store keys offline. These provide the highest level of key protection, making them immune to hackers and viruses, although they can be more complex to use.

How to choose wallet

Now that we have reviewed the main types of crypto wallets, finding the right Bitcoin wallet should be much easier. So, what should you pay attention to when selecting a storage option for your digital assets? Here are the top recommendations:

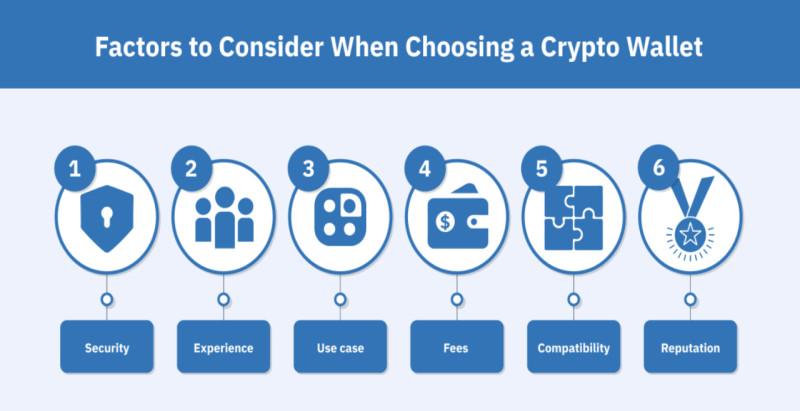

- Determine your needs. Each user has different requirements for storing and using digital currencies. Some need a wallet for everyday transactions like payments or trading, while others are looking for long-term storage of their coins.

- Consider different types of crypto wallets. We have already covered the key features, as well as the advantages and disadvantages, of each wallet. Pay particular attention to security, especially how private keys are protected.

- Check the supported currencies. Different wallets support various types of currencies. Before downloading an app or purchasing a device, ensure that it supports the specific digital coins you need.

- Pay attention to interface usability. To avoid wasting time learning how to use the wallet, it is recommended to choose one with an intuitive interface. This is often a drawback of hardware wallets: they are the most secure but also the most complex to use.

- Ensure the reliability of the developer. The reputation of the wallet’s developer is important for security and functionality. Read user reviews about the software’s ease of use and other key features.

Before making a final decision, it is essential to thoroughly analyze all the wallet’s parameters. It should closely match your priorities and needs while offering reliable protection for your crypto assets.

How to create BTC wallet

As we have established, any transaction involving cryptocurrencies requires a crypto wallet. In this and the following sections, we will take a closer look at how to create and use a Bitcoin wallet.

The process of setting up a digital currency wallet is fairly simple, and even beginners can handle it. It involves the following steps:

- Choosing the type of wallet. The choice depends on the purpose of the wallet: whether it is for everyday use, such as making payments and transfers, or for long-term storage. Hot wallets are more suitable for the former, while cold wallets are recommended for the latter.

- Downloading and installation. Depending on the type of wallet, you can download it from the provider's official website or from an app store on your smartphone. If you opt for a hardware wallet, it is recommended that you purchase it from official stores rather than second-hand sources or online marketplaces.

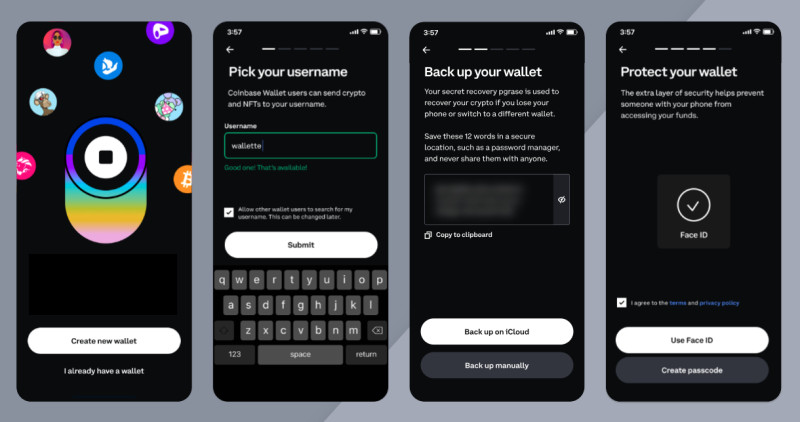

- Setup. After installing the app or program, you will need to create login credentials (username and password). It is also recommended to securely record the recovery phrase provided by the wallet in case you lose access to the device or account.

- Verification. Once the account is created, many platforms, including crypto wallets, require verification, which involves confirming your identity (KYC procedure). This usually involves submitting a copy of your passport or other document with a photo, identification number, and other personal details.

- Setting up two-factor authentication. This security measure requires users to provide two types of data, such as entering a password and then a code sent via SMS or email. It is recommended as an extra layer of protection against potential threats.

- Using the wallet. Once your wallet is set up, you can start using it. In the next section, we will discuss how to use your wallet and explore its features in more detail.

How to use BTC wallet

Now that we have explored the types of wallets and how to create one, let’s delve into how to use it—whether to check your Bitcoin wallet balance, fund it, or withdraw money. We will break down the most popular features in this and the following sections:

- Storage is the most obvious function of a wallet. Keep in mind that cryptocurrency wallets do not actually store digital coins. The coins are stored on the blockchain, and the wallet only holds the keys to manage them.

- Buying and selling crypto – Transactions for purchasing and selling coins are usually conducted on exchanges, through exchangers, or on P2P platforms. These platforms allow for the exchange of fiat money for crypto and vice versa.

- Sending and receiving – To send crypto, you only need to know the recipient's wallet address. This information is not confidential, so you can freely share it with other users.

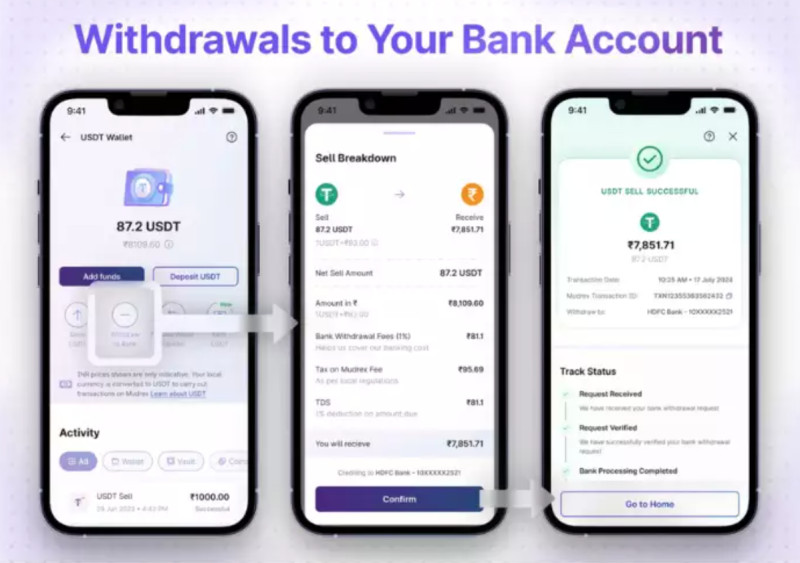

- Withdrawing and cashing out – Once digital currencies are converted to traditional money through exchanges, the funds can be transferred to a bank account. There are also special devices called "crypto ATMs" that allow you to deposit or withdraw cash from your wallet.

- Payments and transfers – Some stores and service providers accept cryptocurrency as a payment method. To complete a purchase, the buyer needs to send the required amount to the seller’s wallet.

Most popular services offering crypto wallets make them multi-currency, meaning you can manage several digital currencies from one app or device. This is convenient as it allows for portfolio diversification. When creating a wallet, it is important to check which coins it supports.

How to deposit and withdraw funds

Let’s assume you already have a wallet. Now it is time to figure out how to fund it and withdraw money. One way is to transfer money to a Bitcoin wallet—anyone who knows the wallet's address can do this. You can also fund your wallet yourself.

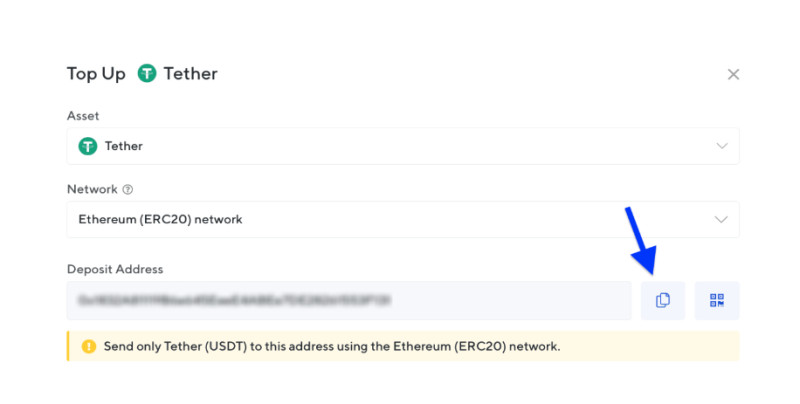

Typically, to fund a wallet for the first time, you will need to exchange fiat money for cryptocurrency. This can be done through various means, including crypto exchanges, exchange services, or P2P platforms. You will need to register on any of these platforms and choose a deposit method.

One of the most popular and easiest methods is to use a bank card. You will need to add the card to your account by providing its details, including the card number, expiration date, and CVV code. The card will also be required to convert crypto back to fiat and withdraw funds.

Once all necessary operations are complete, and you have acquired the desired amount of digital currency, you can transfer it to your crypto wallet for safer storage. However, be aware that transferring money between platforms or from a wallet to an exchange typically incurs transaction fees.

When funding wallets or transferring funds to an exchange, it is crucial to select the correct network (e.g., ERC20, BEP20, etc.). The same cryptocurrency can be supported by different networks, and one network can support multiple currencies. Choosing the wrong network could result in the permanent loss of funds.

Withdrawing funds from a crypto wallet is also straightforward: select the currency you wish to withdraw, enter the address where the funds will be sent, choose the network, and confirm the withdrawal. If you do not plan to continue working with crypto, you can exchange it for fiat and withdraw it to your bank card.

Top BTC wallets

We have already explored the various types of crypto wallets, how to choose them, and how to set them up. Now let’s dive into the question: which is the best Bitcoin wallet? Each wallet comes with its own unique features and offers different levels of security for digital currencies.

For every user, the "best wallet" will vary depending on their needs, such as how often they plan to use their coins, how long they intend to hold them, and more. These questions should be answered in advance to make the right choice.

Undoubtedly, the most critical factor to consider is security, as it directly impacts the safety of your digital assets. Pay close attention to the wallet's developer, its reputation, and the security measures used, such as backup options.

Backup is particularly useful for multi-currency wallets or when users have several wallets. For each individual wallet and digital currency stored within, a separate private key is required. These keys need to be stored securely to avoid loss.

The best wallets support multiple cryptocurrencies, allow for the exchange between different currencies, and provide up-to-date market information, including news. They should also have a user-friendly interface and offer extra features for convenience.

In some wallets, there is an option to adjust transaction fees. Miners prioritize transactions based on the fee offered: the higher the fee, the quicker the transaction is processed.

Another handy feature is the availability of multiple wallet versions for different devices, such as mobile apps and desktop or web versions. This provides access to digital coins anytime, anywhere.

Privacy concerns

When digital currencies first emerged, transactions were completely anonymous—no one could identify the sender or receiver. However, with the rise of centralized platforms, anonymity is increasingly under scrutiny.

As a result, the appeal of using an anonymous Bitcoin wallet has grown among users. But what does that entail, and what sacrifices are made for privacy? The key advantage of such wallets is the ability to perform all digital currency operations anonymously.

Anonymous wallets have the following features:

- Hidden addresses – These one-time-use addresses conceal the recipient's actual address. A new address is generated for each transaction, preventing the operation from being linked to a specific user.

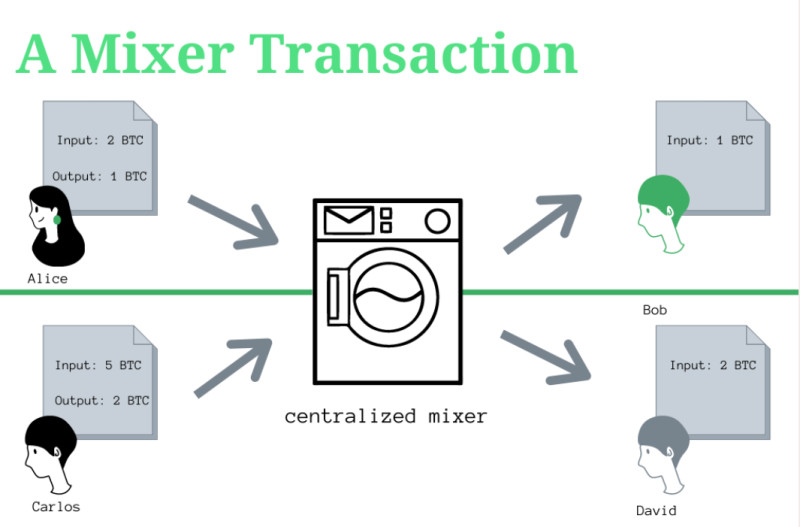

- Coin mixing – Transactions from different users are mixed together, making it harder to trace the source and destination of individual transfers.

- Ring signatures – These allow a user to sign a transaction on behalf of a group, keeping the actual signer hidden. For example, this feature is available on the Monero blockchain.

- VPN integration – By masking IP addresses, this feature provides an additional layer of anonymity.

Enhanced anonymity helps protect users' personal information and financial history. Their transactions are nearly impossible to trace, reducing the likelihood of data being used against them. This is particularly important for large holders of cryptocurrency, often referred to as "whales," who are more vulnerable to hacking attempts.

Privacy is also essential for businesses that accept crypto payments. To maintain a competitive edge, companies must ensure privacy to prevent sensitive commercial strategies from being exposed, which could negatively impact profits.

However, it is important to consider the ethical implications. Criminals engaged in money laundering or financing terrorism also rely on anonymity. The reduction of privacy in blockchain systems is partly a response to combat such illegal activities.

Bitcoin wallet: tips for safe usage

Creating a wallet to store your virtual money is just the first step. It is crucial to follow necessary security measures to ensure the safety of your cryptocurrency. Here are some important recommendations for using crypto wallets securely:

- Choose a reputable developer. Make sure to research user reviews not only about the wallet’s functionality but also about its developers. The most important factor to focus on is the security measures implemented in the wallet.

- Strengthen your security. Use strong, complex passwords when creating your account. In addition, enable two-factor authentication (2FA) for an extra layer of protection, which requires a one-time password or a code from another app.

- Use backup options. Backup features will help save all your data and passwords in case of loss. This ensures you will not lose access to your wallet or your digital coins.

- Store private keys separately. Without the private key, you will not be able to perform any actions with your cryptocurrency. Losing these keys can mean losing access to your funds entirely. A good option is to write the keys down on paper and store them in a secure location.

- Keep your seed phrase safe. A seed phrase is used to restore access to your wallet and funds if you lose your password or private key. However, this may not apply to hardware wallets.

- Regularly update your wallet. This primarily applies to online, desktop, and mobile wallets. Regular software updates ensure better protection against hacking and other attacks.

- Store large amounts in cold wallets. Since hot wallets are more vulnerable and may become targets for cybercriminals, keeping digital coins in cold wallets offers greater security for long-term storage.

Conclusion

In this article, we have explored what a Bitcoin wallet is, its various types, how to create one, and how it is used. It is important to understand that a crypto wallet does not store the digital coins themselves, but rather the keys that grant access and control over your assets.

The most common classification of wallets divides them into cold and hot wallets. The former are external devices, such as USB drives, that are not connected to the Internet and provide more secure storage. The latter are software-based and are more suitable for everyday use.

Each wallet has two keys: a public key and a private key. The public key is the wallet address and can be shared with others to receive payments. The private key, on the other hand, is confidential and should never be shared, as it provides access to the coins in the wallet.

When creating a wallet, pay attention to the developer’s reputation and read user reviews. It is also recommended that you set up two-factor authentication, backup features, and other security measures to protect your crypto assets from criminal threats.